This article is adapted from China Playbook, our subscription-based strategy hub for decision-makers navigating China’s ever-shifting consumer landscape.

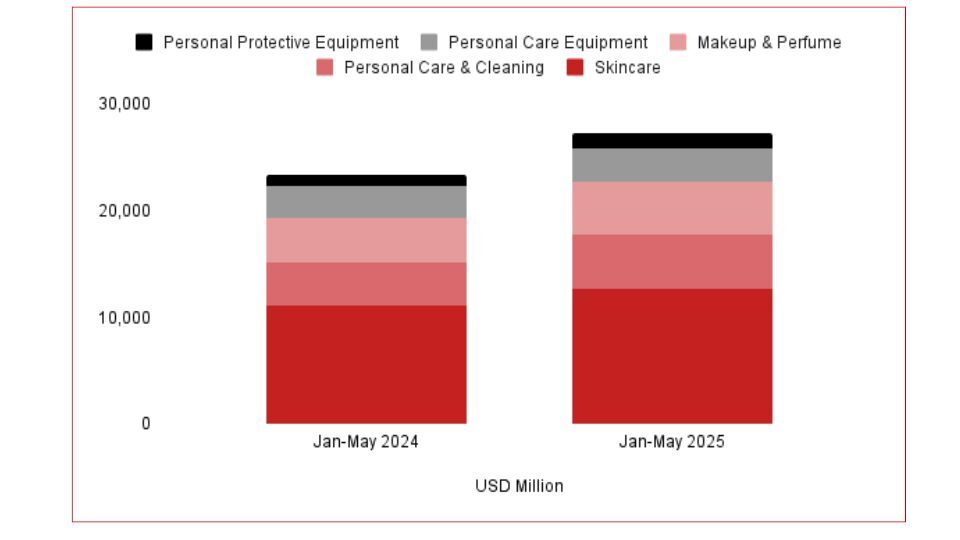

China’s beauty sector saw 17% overall growth from January to May 2025 compared to the same period in 2024, with net sales across Tmall, JD.com and Douyin reaching $27.3 billion.

What’s Driving the Growth?

-

Skincare remains dominant, contributing nearly half of all sales at $12.6bn (+14% YoY).

- Personal Protective Equipment was the standout, up 44% YoY to $1.5bn.

-

Makeup & Perfume hit $4.9bn (+17% YoY).

-

Personal Care Equipment grew more modestly at $3.1bn (+6% YoY).

Brand And Product Highlights

-

Facial Skincare Sets remained the top-selling product type, generating $3.2bn in sales (+11% YoY). Local player Kans 韩束 led the pack, with $315m in sales across Jan–May 2025, including $63.5m on Douyin alone.

-

Local brand Proya 珀莱雅 was the best-performing brand overall, with $466m in skincare sales, despite a slight decline of -3.2% YoY.

-

L’Oréal ranked third overall and stood out as the best-selling global brand, with $425m in sales (+0.1% YoY).

The Pricing Picture

Consumer behaviour points to a polarised market:

-

Premium products ($50+) made up 44% of skincare sales and were the second-fastest growing segment (+16% YoY).

-

Entry-level products (below $10) grew the fastest (+20% YoY), though from a smaller base at just 11% share.

This dual trend suggests that while many consumers are trading down in search of value, others are actively trading up for premium quality — leaving the middle segment squeezed.

What This Means For Brands

China’s beauty market remains one of the most dynamic globally. Local players like Kans and Proya continue to dominate through strong digital execution and resonance with younger consumers, while global giants like L’Oréal still hold relevance but face a more competitive landscape.

The key for brands? Recognise market polarisation and respond with clear, segmented strategies. Value-driven offerings and premium innovations both have room to grow — but the middle ground is increasingly a tougher sell.

Are you ready to unlock your unfair advantage in China?

This article is adapted from our subscription-based strategy hub, China Playbook. Read the full article here with insights and takeaways from our senior strategist, or click the button below to subscribe for free updates.

Cover image collaged via Tmall

Related blog posts

.jpg?width=1920&height=1080&name=China%20Playbook%20cover%20(2).jpg)